Our weekly roundup of news from East Asia curates the industry’s most important developments.

Blowing up a Singaporean crypto hedge fund worth an estimated $10 billion at its peak was, by all means, a life-changing event for its co-founders Kyle Davies and Zhu Su. It appears that the trauma from the incident had been so severe that the two executives embarked on a series of spiritual journeys starting mid-2022 to transcend the effects of Three Arrow Capital’s (3AC) bankruptcy.

The voyage appears to have been fruitful. From escaping the pursuit of creditors, to making philosophical observations after witnessing the deaths of German tourists, to discovering the grace of Allah through Islam, to reigniting their passion for life through the culinary arts, to finding companionship in Japanese NFT avatars, Davies and Su may have finally found the answer to overcoming life’s hardships: If you don’t get it right the first time, keep trying until you succeed.

After reportedly soliciting $25 million from investors in January, the former 3AC co-founders launched the OPNX exchange on Apr. 5. The exchange is designed to trade bankruptcy claims of fallen crypto entities, such as their own bankrupt hedge fund. It is unclear how the highly personalized and private nature of bankruptcy claims can allow them to be traded on a public exchange without prior approval from bankruptcy trustees or courts.

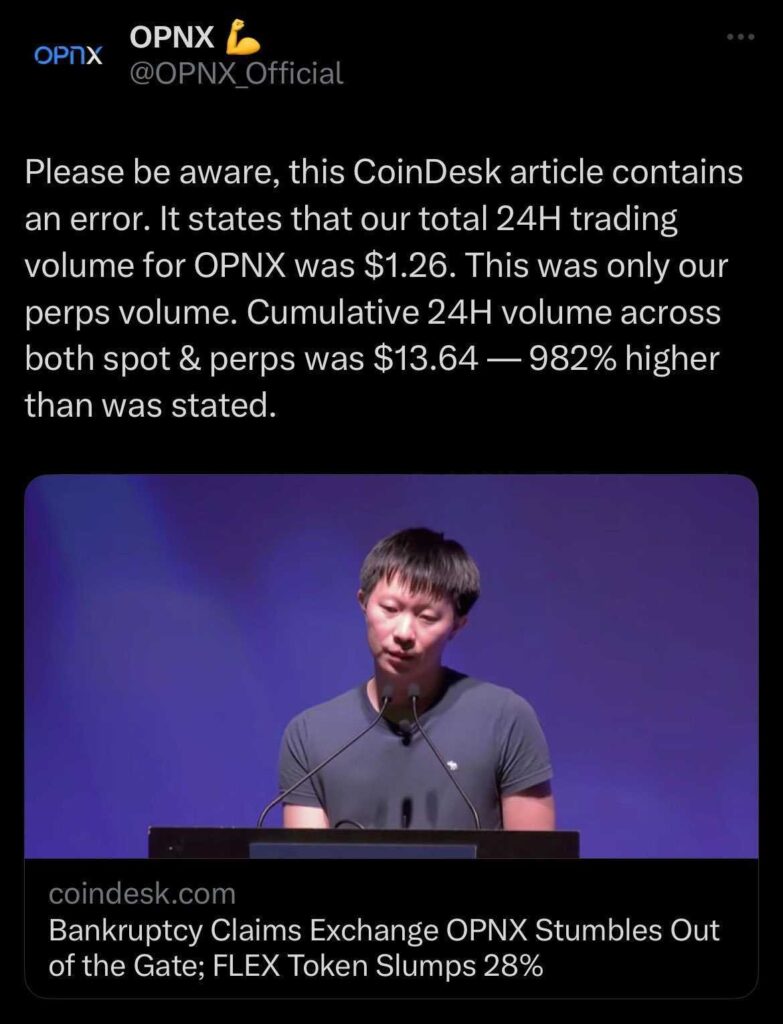

Nevertheless, Davies and Su decided to press forward with the idea anyway. On the first day of trading, the total trading volume on OPNX in the previous 24 hours was reportedly $1.26. The report drew swift condemnations from OPNX, which clarified that the exchange’s 24-hour trading volume was actually $13.64, or 982% more than stated.

On the second day, Zhu Su claimed that the exchange facilitated $373 in trading volume after a media blitz brought much attention to the lackluster results. However, with great power comes great responsibility. Despite improving the exchange’s trading volume by 2,634% in one day, OPNX’s traction was partly derailed by Twitter suspending its official account due to terms of use violations.

Su has since created a Chinese Telegram channel for official OPNX communications. Meanwhile, the two were kindly reminded by critics once again that despite their continued entrepreneurship, creditors are still claiming an estimated $3.5 billion from their defunct hedge fund.

Huobi’s liquidation controversy

In a letter submitted to Chinese news aggregator Odaily.news, cryptocurrency exchange Huobi Global appears to have presented its side of the story regarding a flash crash that affected its native Huobi Token (HT) on Mar. 10.

On the date of the incident, HT plunged to as low as $0.31 apiece from a high of $4.85 before subsequently recovering most of its losses. It currently trades at $3.58 at the time of publication.

According to Huobi, the incident was caused by “industry-wide macro events” relating to the recent failure of American tech banks. “Under such downward pricing pressures, repeated selling by big investors, and lack of liquidity with the HT token, led to margin liquidations, and in turn caused many leveraged investors to suffer losses,” Huobi wrote.

The event led to big losses among users who pledged HT as collateral for loans or were simply holding the token with leverage. Amid the guidance of self-proclaimed “adviser” and de facto owner of Huobi, Justin Sun, Huobi rolled out a compensation program for users affected by the HT flash crash and claimed that “more than 98% of affected users have negotiated a satisfactory solution with the platform and received compensation.”

However, one user, @lantian666, who claims to have lost nearly $4 million during the incident, alleges that his losses are yet to be fully compensated by Huobi. In the Odaily letter, Huobi acknowledged that one user lost an estimated $2.9 million after the flash crash caused liquidations. lantian posted a series of screenshots and claims that Huobi’s customer service had only agreed to waive a portion of liquidation fees, which are nowhere close to his loss on trading positions.

Sun has stated that Huobi will “bear all leverage-through position losses on the platform resulted from this market volatility event of HT.” Huobi has stated that it seeks to “reach a consensus as soon as possible with the remaining users who still have doubts about the current solution and negotiate a more satisfactory solution.” However, the exchange also wrote it did not want such compensation to “encourage users to engage in high-risk leveraged transactions.”

Justin Sun’s troubled acquisition

According to purportedly leaked employee screenshots on Apr. 4, Huobi Global plans to cut it staff count by a further 200 and the exchange is apparently not yet profitable. Last November, blockchain personality and Tron founder Justin Sun reportedly acquired 100% of a co-founders’ stake in the exchange through his entity About Capital.

There have been issues ever since — but the exchange had issues before as well. Early this year, Huobi reportedly slashed its employee benefits and laid off as much as 20% of its staff. The exchange’s market share had fallen from an estimated 5.4% in the first quarter of 2022 to 2.2% in the final quarter. On Apr. 5, Sun denied that he was in talks to sell his Huobi stake to Binance.

Huobi was one of the largest cryptocurrency exchanges in the world, holding 19% market share in 2020 before China’s crypto exchange ban took effect and it had to say goodbye to much of its userbase. Sun apparently has a plan to get around the ban as part of its turnaround. The proposed scheme involves leveraging Huobi’s digital identity partnership with the Carribean island of Dominica. Mainland Chinese users can register for Dominica’s digital citizenship, then reportedly use their new “citizenship documents” to create a Huobi account.

Sun is currently facing a lawsuit from the U.S. Securities and Exchange Commission over allegations of market manipulation related to the Tron and BitTorrent tokens. Recent reports also suggest that Sun was stripped of his status as Grenada’s ambassador to the World Trade Organization in June 2022, depriving him of the fancy title “his excellency” and access to a diplomatic passport which grants him theoretical immunity against prosecution.

Microsoft’s new blockchain partnerships

According to a recent announcement, Singaporean gaming studio Metagame Industries has joined the Microsoft for Startups Founders Hub through the ID@Azure Program. The partnership with Microsoft will explore the use of AI and cloud computing in Web 3.0 game development.

Metagame Industries will receive Azure credits, OpenAI Services, technical support, and business development resources as part of the agreement. “We’re excited to work with Microsoft’s tools and technology to create innovative and immersive gaming experiences,” said Joe Zu, CEO of Metagame Industries.

The firm is the developer behind Abyss World, a third-person, dark fantasy action role-playing game scheduled to launch on Mysten Labs’ Sui blockchain in Q4 2023. Abyss World will feature an in-game NFT factory that enables the minting of digitized weapons and heroes via monster drops.

Token rewards will also be available to players who complete special tasks in the PvE section, climb the game leaderboard, and win PVP arena seasons. Developers also plan to implement an Abyss World decentralized autonomous organization (DAO) to regulate game tasks such as new systems and introduction of new character sets.

Asia Express previously reported that Microsoft has partnered with decentralized blockchain infrastructure provider Ankr on Microsoft Azure. Rashmi Misra, Microsoft’s general manager of artificial intelligence and emerging technologies, commented that its partnership with Ankr will allow projects to access “blockchain data in a reliable, scalable, and secure way.” The tech conglomerate is also reportedly testing a Web 3.0 wallet integration for its native internet browser Microsoft Edge.