Swedish crypto tax firm Divly has released a new report that estimates that only 0.53% of crypto investors globally paid tax on their crypto in 2022 — however tax experts have cast doubt on the figures and methodology.

The Divly report published on April 5 came up with the estimate after analyzing the relationship between the number of people who declared cryptocurrency in their tax returns, and the search volume for crypto tax-related keywords in various countries. It also used the number of crypto holders in each country according to Statista‘s Global Cryptocurrency Report in its calculations

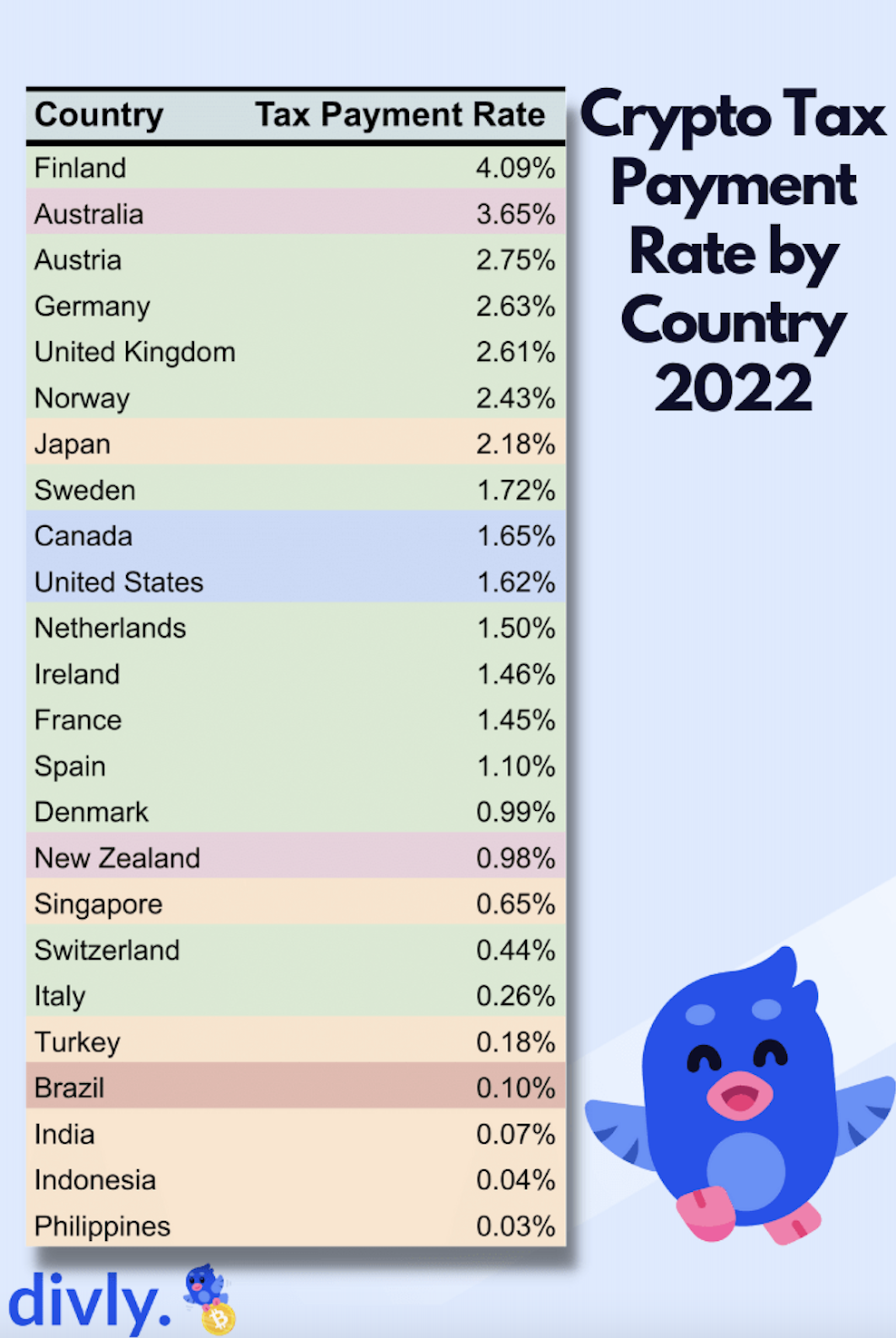

The report estimates that Finland has the highest proportion of crypto investors who paid the required taxes on crypto in 2022 at 4.09%, with Australia following closely behind on 3.65% respectively.

The United States ranked 10th on the list, with an estimated 1.62%, meanwhile, India, Indonesia and Philippines had the lowest rates of tax-paying crypto investors, with just 0.07%, 0.04% and 0.03% respectively.

The methodology used to arrive at the estimates is questionable. The report itself qualifies the results by noting that search volume data may not accurately reflect the actual number of crypto taxpayers, as not everyone who pays tax searches for crypto tax-related information online.

Another assumption in the methodology was that the number of searches related to crypto tax reporting did not vary across different countries. Additionally, it cautioned that there could be a potential bias towards countries with greater internet accessibility and more accurate search volume data.

Danny Talwar, global head of tax at crypto tax software Koinly, disputed the large portion of crypto investors not paying tax that the report suggests. He told Cointelegraph:

“It is likely that 99.5% is not reflective of countries that have specific crypto tax guidance and strict compliance requirements such as USA, Canada, Australia and India.”

Chartered Accountant Greg Valles, a board member of Blockchain Australia, also said he would not be able to “say conclusively that the methodology is 100 percent accurate.”

Both tax specialists noted government data matching and surveillance efforts meant it was getting progressively more difficult to avoid crypto taxes.

Valles said that as government technology gets more sophisticated and specialized, it will become easier to detect anyone that is not complying and warned that those who fail to report their crypto profits now, risk it catching up with them in future years.

Related: Biden’s policy on crypto taxation undermines his environmental goals

Talwar emphasized that although the risk of non-compliance for crypto is comparatively higher than other asset classes, tax authorities in many countries have processes in place to obtain data from crypto exchanges.

He added that Koinly has seen awareness in crypto tax “increase considerably” amongst investors in these jurisdictions, with only “15% of surveyed crypto investors” being unaware of their crypto tax reporting duties.

Magazine: Best and worst countries for crypto taxes – plus crypto tax tips